Due to the rapid increase in market price of iron ore in the early period, steel mills continued to increase the ex-factory prices of finished products. At the same time, due to expectations for the spring market, the willingness of traders to increase their winter deposits, and the domestic steel market, there are also pre-planned pull-up habits. The short-term overall domestic steel market will increase steadily.

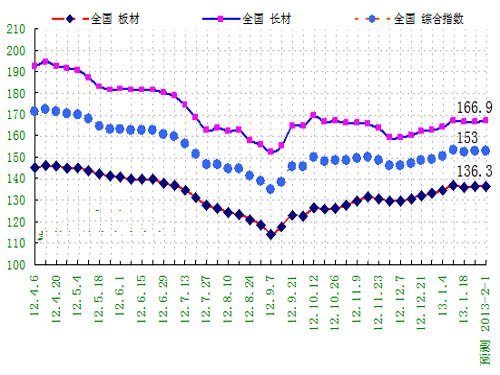

Due to the rapid increase in market price of iron ore in the early period, steel mills continued to increase the ex-factory prices of finished products. At the same time, due to expectations for the spring market, the willingness of traders to increase their winter deposits, and the domestic steel market, there are also pre-planned pull-up habits. The short-term overall domestic steel market will increase steadily. According to the Lange Steel Information Research Center weekly price prediction model data, this week (2013.1.28-2.1) domestic steel market prices will be slightly higher, the long products market will pull up slightly, while the plate market prices will be steadily increased. The Lange Steel Composite Index is expected to fluctuate around 153 points, the average price of steel is around 3980 yuan, and the average volatility is about 30 yuan. Lange Steel's long product index is expected to fluctuate around 166.9, and it will be pulled up by about 0.5 point. The steel sheet price index of Georgia is expected to fluctuate around 136.3 points, and it will be about 0.1 point higher.

From the market research of Lange Steel Information Research Center, it is expected that the domestic long product market price will increase slightly this week (2013.1.28-2.1), and the plate market price will increase steadily; raw material market prices will rise and fall. The market price of iron ore and coke will remain stable, the market price of scrap will drop by 50-60 yuan, and the billet market price will rise by 30-60 yuan.

1. Domestic steel market slightly increased this week. Week 4 of 2013 (2013.1.21-1.25) Lange Steel (LGMI) Composite Price Index reached 152.7 points, a week-on-month increase of 0.12%, and a decrease of 8.94% from the same period of last year. Among them, the LGMI long products price index was 166.4 points, a week-on-month increase of 0.13%, a decrease of 12.29% from the same period last year; LGMI sheet price index was 136.2 points, a week-on-month increase of 0.11%, a decrease of 3.52% over the same period last year.

According to the market monitoring of Lange Steel Information Research Center, the price changes of 17 types of 44 steel products and steel products in some parts of the country during the fourth week of 2013 (2013.1.21-1.25) are as follows: Major steel product markets Prices rose slightly, compared with last week, rising varieties increased significantly, flat varieties increased, and declined varieties decreased significantly. Of these, 19 varieties rose, 12 more than last week; 17 were flat, 6 more than last week; 8 products fell, 18 less than last week. The domestic iron and steel raw materials market prices were mixed, iron ore market prices rose steadily by 40 yuan, coke market prices rose steadily by 20 yuan, scrap market prices fell by 30-70 yuan, billet market prices fell by 10 yuan.

2. The national steel social stocks have slowed down this week. At present, the nation's steel stocks have rebounded for 5 weeks. The rise in building materials and sheet stocks have all slowed. According to market monitoring by Lange Steel Information Research Center, on January 25th, steel society stocks in 29 key cities across the country were 13.3 million tons, an increase of 281,100 tons from last week, which was an increase of 2.17%, and a slower growth rate of 1.33 from the previous week. Percentage. From the perspective of sub-categories, the country’s social inventory of wire rods was 1,139,600 tons, up 1.69% from last week; rebar social stocks were 5,468,600 tons, up 3.95% from the previous week; the inventory of social stocks of disk tigers was 376,800 tons. This was an increase of 3.26% from last week; the social volume of hot coiled coils was 3,290,600 tons, up 1.42% from the previous week; the social volume of cold-rolled coils was 15,195,500 tons, 0.20% lower than last week; the plate's social inventory The amount was 1,327,900 tons, a decrease of 0.17% from the previous week.

3. This week, the steel market fluctuates and rises. In the fourth week of 2013 (2013.1.21-1.25), the thread ** continued to rise, accompanied by an increase in volume. This week's weekly closing price rose by 74 points or 1.85% from the previous week. This week, the main contract holds 1.579 million contracts, and the increase in the number of warehouses has reached 289,000. While the position has increased substantially, the transaction volume has also increased by 800,000 hands.

4. Concern about the recent factors affecting steel prices Macroeconomics:

The State Council issued the Twelfth Five-Year Plan for the Development of the Marine Economy of the State Council. The National Twelfth Five-Year Plan for Marine Economic Development issued by the State Council recently stated that China's marine science and technology innovation capability has been further strengthened during the Twelfth Five-Year Plan period, and the rate of conversion of marine scientific and technological achievements in 2015 has reached More than 50% of the marine science and technology contribution to the marine economy has reached more than 60%. The capacity for sustainable development of the ocean has been further enhanced. 80 new types of marine protection zones were established at all levels. In 2015, the proportion of marine protected areas in the jurisdictional sea area reached 3%. The plan also proposes that the structure of China's marine industry will be further optimized during the "12th Five-Year Plan" period, and breakthroughs will be made in emerging marine industries. In 2015, the value added will more than double from the end of the "Eleventh Five-Year Plan" period, accounting for more than 3% of the total value of marine production; The average value-added of marine service industry has increased by 9% annually, and its share in the total value of marine production has continued to increase.

At the same time, the plan calls for the further improvement of China's marine economic control system during the “12th Five-Year Plan†period and the marked increase in the level of opening to the outside world. The plan proposes to give full play to the leading role of the three economic zones in the Bohai Rim, the Yangtze River Delta, and the Pearl River Delta, promote the formation of three marine economic circles in the north, east, and south of China, combine the implementation of national deployments on the development of coastal areas, and focus on cultivating a number of important Marine economic growth pole.

The State Council issued the “Twelfth Five-Year Plan for Energy Development†on the 23rd of the State Council’s General Office of the State Council. The plan released the main goals of energy development in 2015, including total energy consumption and efficiency, energy production and supply capacity and Other aspects. The notification required that in 2015, the implementation of dual control of energy consumption intensity and total consumption was required, total energy consumption was 4 billion tons of standard coal, electricity consumption was 6.15 trillion kwh, and the energy consumption per unit of GDP was 16% lower than in 2010. . The overall energy efficiency has increased to 38%, the standard coal consumption for thermal power supply has dropped to 323 g/kWh, and the comprehensive processing energy consumption for refining has dropped to 63 kg standard oil/ton.

It is required to speed up the construction of comprehensive energy bases in Shanxi, Ordos Basin, East Inner Mongolia, Southwest China and Xinjiang. By 2015, the five major bases will have a primary energy production capacity of 2.66 billion tons of standard coal, accounting for more than 70% of the country's total output; 1.37 billion tons of standard coal will be output externally, accounting for 90% of the national trans-provincial transportation volume.

The Ministry of Industry and Information Technology issued the "Guidance Opinions on Accelerating the Promotion of Mergers and Reorganizations in Major Industries"

In order to promote the merger and reorganization of enterprises, increase industrial concentration and cultivate a number of large-scale enterprise groups with international competitiveness, the Ministry of Industry and Information Technology, the Ministry of Finance, the National Development and Reform Commission, the Securities Regulatory Commission and other departments jointly issued on the 22nd “on accelerating the promotion of mergers and acquisitions of enterprises in key industries. "Guiding Opinions" (hereinafter referred to as the "Guiding Opinions"), the comments pointed out that through the promotion of mergers and reorganizations of enterprises, the degree of industrial concentration was increased, large-scale and intensive management was promoted, market competitiveness was enhanced, and a group of large-scale enterprise groups with international competitiveness were cultivated. Promote the optimization and upgrading of industrial structure; further promote enterprises to change operating mechanisms, strengthen and improve internal management, improve corporate governance structure, establish a modern enterprise system; accelerate the strategic adjustment of the layout and structure of state-owned economy, promote the development of non-public economy and SMEs, and improve The basic economic system with public ownership as the main body and a variety of ownership systems for common development.

The guidelines clarify the goal of the merger and reorganization of the steel industry, that is, by 2015, the industry concentration of the top 10 iron and steel enterprise groups will reach around 60%, and 3-5 companies with core competitiveness and strong international influence will be formed. 6-7 enterprise groups with strong regional market competitiveness. The guiding opinions also stated that the major support for large iron and steel enterprise groups is to implement cross-regional and cross-ownership mergers and reorganizations. Actively support regional advantages and mergers and acquisitions of iron and steel enterprises. Significantly reduce the number of companies and increase the concentration of the steel industry. Support the restructured steel companies to carry out technological transformation, eliminate backward production capacity, optimize regional layout, and increase market competitiveness. Encourage steel companies to participate in mergers and acquisitions of foreign steel companies. In addition, the guidance also encourages steel companies to extend the industrial chain. The focus will be on supporting the integration of existing iron and steel enterprises in the country's existing mine resources and coking enterprises, and encouraging steel companies to reorganize domestic scrap processing and distribution companies that meet environmental protection requirements.

HSBC China January PMI preview value 51.9 hit a 24-month high 24 HSBC Bank released data show that China's January 2013 manufacturing purchasing managers index (PMI) preview value of 51.9, last year's December final value of 51.5. Following the return to the 50-pounding watershed in November last year, the index recovered further from the previous month's 51.5, hitting a 24-month high. HSBC China Manufacturing PMI is a comprehensive index based on five individual indicators. The indicators and their respective weights are: new orders 0.3, output 0.25, employment 0.2, supplier supply time 0.15, purchase inventory 0.1, including The goods time index is reversed to make its comparability consistent with other indicators. In January, the HSBC China Manufacturing PMI's preview value rose for the fifth straight month and hit its highest level in 5 years at 51.9. This indicates a good start for the new year. Benefiting from the continued growth of new businesses, manufacturers have expanded recruitment and raw material procurement and accelerated production. Although external demand is still lacking, domestic demand-led inventory replenishment will help China's economic recovery in the coming months.

Raw material supply:

According to the Ministry of Land and Resources, 2012 is a year in which the completion of the special three-year target task for geological and mineral surveys and assessments is achieved. In the past three years, geological surveys have achieved a series of results. The central government has invested a total of 17.5 billion yuan, which exceeds the total investment of 12 billion yuan in 12 years of the special survey of land resources. Large input brings large output. In 2012, the newly added resource reserves amounted to 132 billion tons of coal, 5.4 billion tons of iron ore, 100 million tons of manganese ore, 2.36 million tons of copper, 4 million tons of lead and zinc, and 700 million tons of bauxite ore. , Nickel 370,000 tons, tungsten (WO3) 200,000 tons, molybdenum 1.55 million tons, gold 604 tons.

BHP Billiton's 2012 Iron Ore Production Increases 7.6%

Australian mining giant BHP Billiton announced that iron ore production in the fourth quarter was 42.19 million tons, up 3% year-on-year, exceeding expectations. In the second half of 2012, iron ore production increased by 2% year-on-year to 81.926 million tons, and annual production was 160 million tons. , an increase of 7.6%.

Industry News:

The U.S. decided to impose double counter-tariffs on China's application of wind towers to the United States. The US International Trade Commission made a final ruling on the 18th that China's application of wind towers to the United States caused "substantial damage" to U.S. industries, according to which the U.S. will levy products from China. Anti-subsidy and anti-dumping "double reverse" tariffs. According to the announcement issued by the US International Trade Commission, in the 18th vote, three members voted in favor, three members voted against the vote, and there was a dramatic vote. However, in the end, China’s application of the wind tower to the U.S. industry was still recognized. Cause "substantial damages." According to the U.S. trade remedy procedure, after the U.S. International Trade Commission made a definitive final ruling, the U.S. Department of Commerce is scheduled to issue anti-subsidy and anti-dumping orders to the Customs in February of this year, and begin to impose "double countervailing measures" on China's application of wind towers to the United States. tariff.

China Steel Association expects global steel demand to increase by 3.2% in 2013

In the market analysis released on January 21, the China Iron and Steel Association predicted that the global economic situation in 2013 will be better than last year, and the steel demand situation will also be improved. Global steel demand in 2013 is expected to grow by 3.2%, 1.1 percentage points higher than last year. China is affected by the acceleration of economic growth, and it is expected that steel demand will increase by 3.1%, which is an increase of 0.6 percentage points from last year's growth rate. This year's global economic growth rate is expected to be better than last year, and steel demand will also increase. In the new year, the rapid rise in the prices of raw materials will promote the recovery of steel prices. In addition, steel inventories have continued to decrease, market pressure has eased, and they have also played a supporting role in foreign steel prices. Regarding the trend of steel prices in 2013, the Steel Association also put forward three areas that need to be focused on. First, steel production still maintains a high level, the market is still in a situation where supply exceeds demand, and steel production maintains a high level, which is not conducive to a further rise in steel prices. .

In mid-January, daily output of crude steel fell by 1.53%

According to the statistics of the China Iron and Steel Association, the average daily output of crude steel for key large and medium-sized enterprises in mid-January was 1.615 million tons, a decrease of 3.73% compared with the previous period. In the middle of January, the daily output of crude steel in the country reached 1.914 million tons, which fell by 1.53% compared with the previous period.

The previous session of the thread ** rose on the 25th main contract rose 0.99%

In the previous period, the main rebar 1305 contract opened slightly higher at 4040 in early trading on the 25th, and the opening price continued to fluctuate in the late period. Although there was a sharp drop in the intraday price, the overall trend in the day continued to rise. The highest intraday 4085, to close at 4076, compared with the previous trading day (24th) settlement price rose 0.99%, holding positions increased by 145254, the whole day turnover of 3541296 hands.

Downstream demand:

New orders received in 2012 dropped by more than 40% year-on-year. According to the statistics of the Ministry of Industry and Information Technology, from January to December 2012, the total shipbuilding completed nationwide amounted to 60.21 million dwt, which was a decrease of 21.4% year-on-year, of which sea vessels were 19.01 million corrected tons The number of orders for new vessels took a total of 20.41 million dwt, a year-on-year decrease of 43.6%, of which sea vessels were 8.69 million corrected gross tons. As of the end of December, the number of handheld ship orders was 106.95 million dwt, which was 28.7% lower than the end of 2011, among which sea vessels were 36 million corrected gross tons, and export ships accounted for 82.7% of the total.

Global new orders received during the year fell by 45% year-on-year

According to statistics, in 2012, there were only 48.48 million DWT new orders worldwide, a 45% year-on-year decline. Although new orders were picked up in December, there was still a certain gap compared to previous years, indicating that although the shipping market picked up, it did not recover overall. In December, orders received from China and South Korea rebounded sharply. In December, new orders received by China, South Korea, and Japan were 2.24 million, 2.73 million, and 800,000 DWT, respectively. Except for Japan and South Korea, orders from both China and South Korea increased at a larger rate. Although orders from China and South Korea rebounded sharply, they were still weaker than in previous years. Therefore, we believe that the short-term weakness of the shipping market will not change. Three major shipbuilding countries continued to decline in handheld orders. In December, China, South Korea and Japan held orders of 110 million DWT, 69 million DWT, and 58 million DWT, respectively, down 37%, 41%, and 25% year-on-year.

Pot Filler,Kitchen Faucet Pot Filler,Wall Mounted Folding Faucet,Wall Mounted Kitchen Faucet

kaiping aida sanitary ware technology co.,ltd , https://www.kpaidafaucets.com